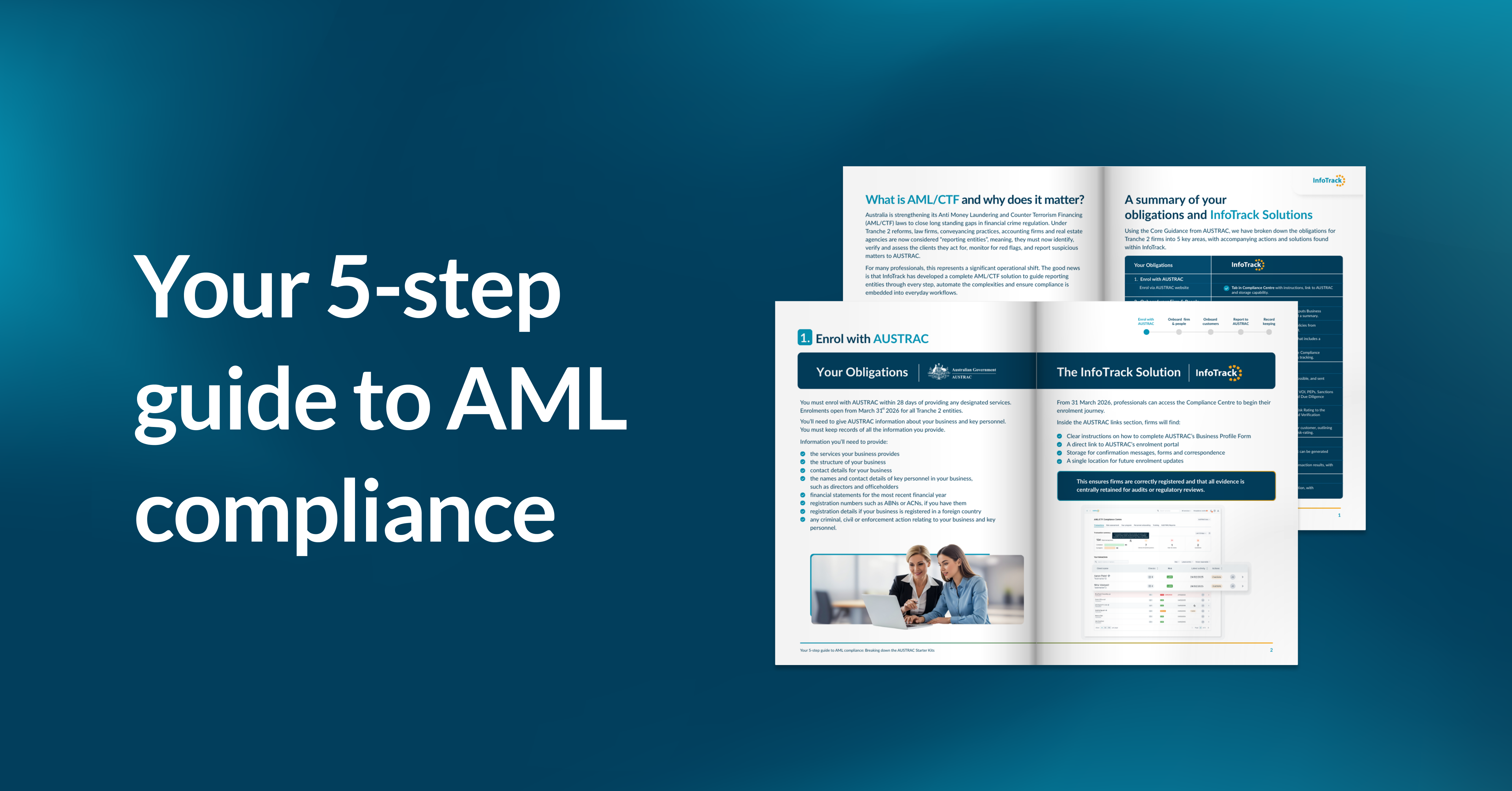

Tranche 2 is the next phase of AML/CTF regulatory obligations in Australia, coming into effect in 2026. It expands compliance requirements to cover additional professionals and activities that were not fully included under Tranche 1. This includes certain property transactions, complex onboarding of clients, and reporting obligations when handling client money. Professionals captured under Tranche 2 include lawyers, conveyancers, accountants, and real estate agents involved in these activities. Organisations must ensure they meet these requirements to remain compliant with AUSTRAC regulations.