Compliant client onboarding and identity verification

Complimentary, all-inclusive AML/CTF solution

Order all your searches and certificates in one place

A dynamic, matter specific environment

Manage family law matters with one solution

Simplify estate administration and planning

Review contracts faster with AI-assisted precision

Electronically lodge registry documents and settlements

Securely collate client financial documentation

Serve documents fast with tracking

Practice Management Integration

Streamline administrative tasks and optimise workflows

Access our support guides for comprehensive self-help assistance

Allows suppliers to connect their products and services with the InfoTrack Ecosystem

Learn how software and integrations can transform the way you work

Find out the latest industry updates

Take on compliance with confidence

Take your professional development to the next level

Cyber Security Awareness Training

Build your cyber resilience

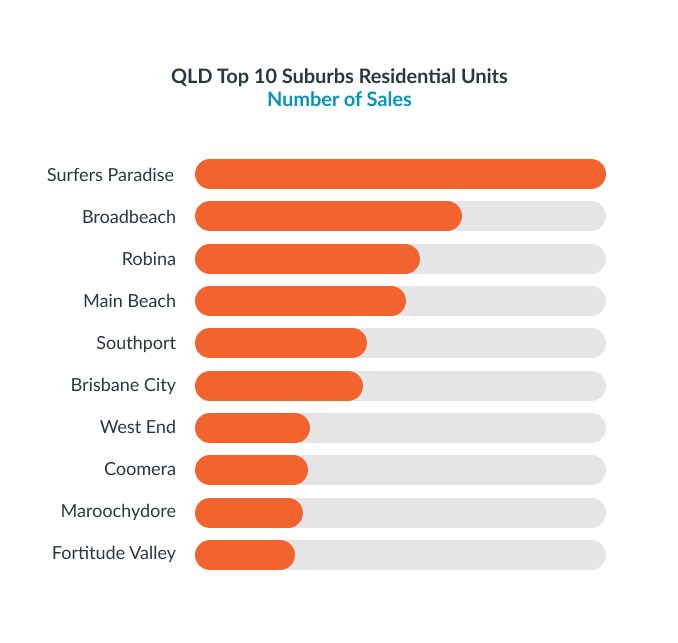

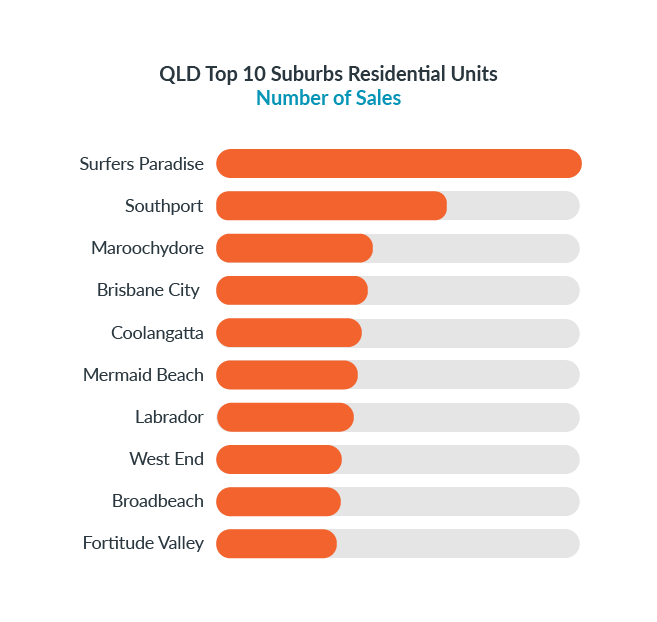

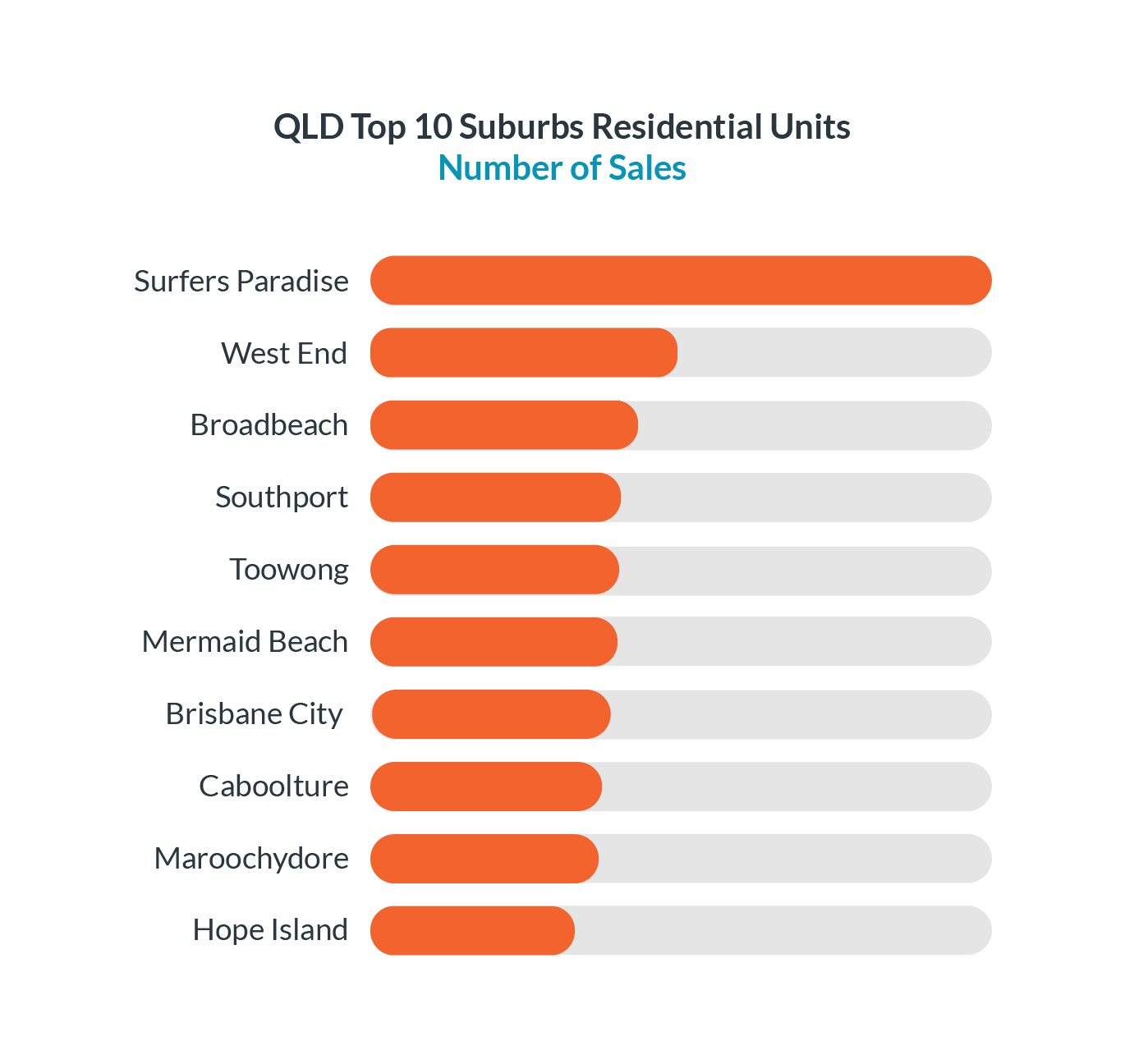

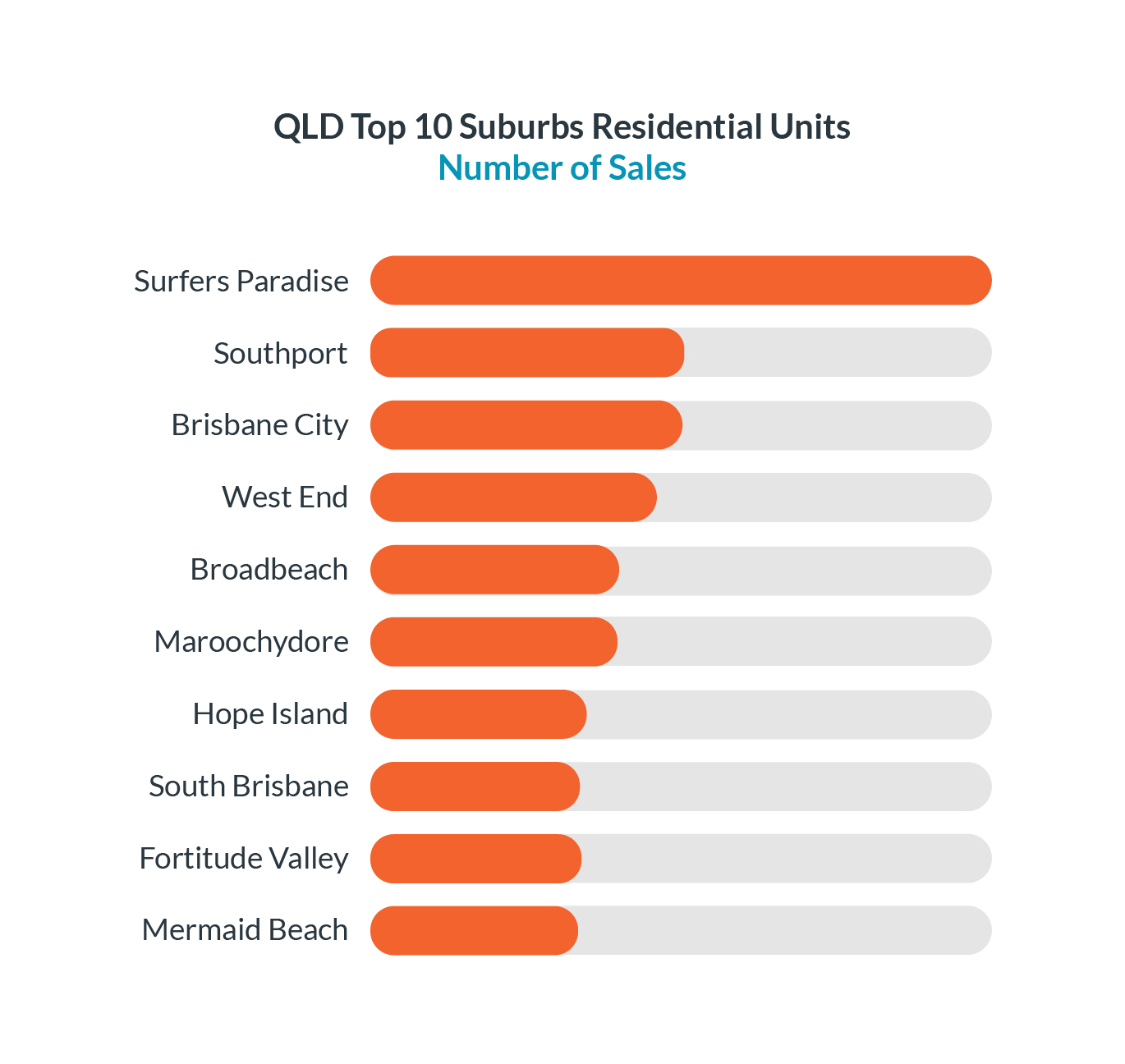

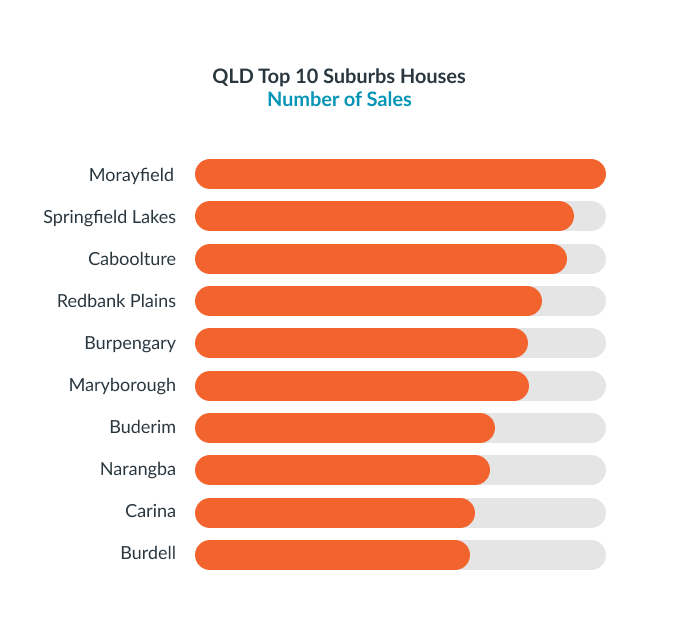

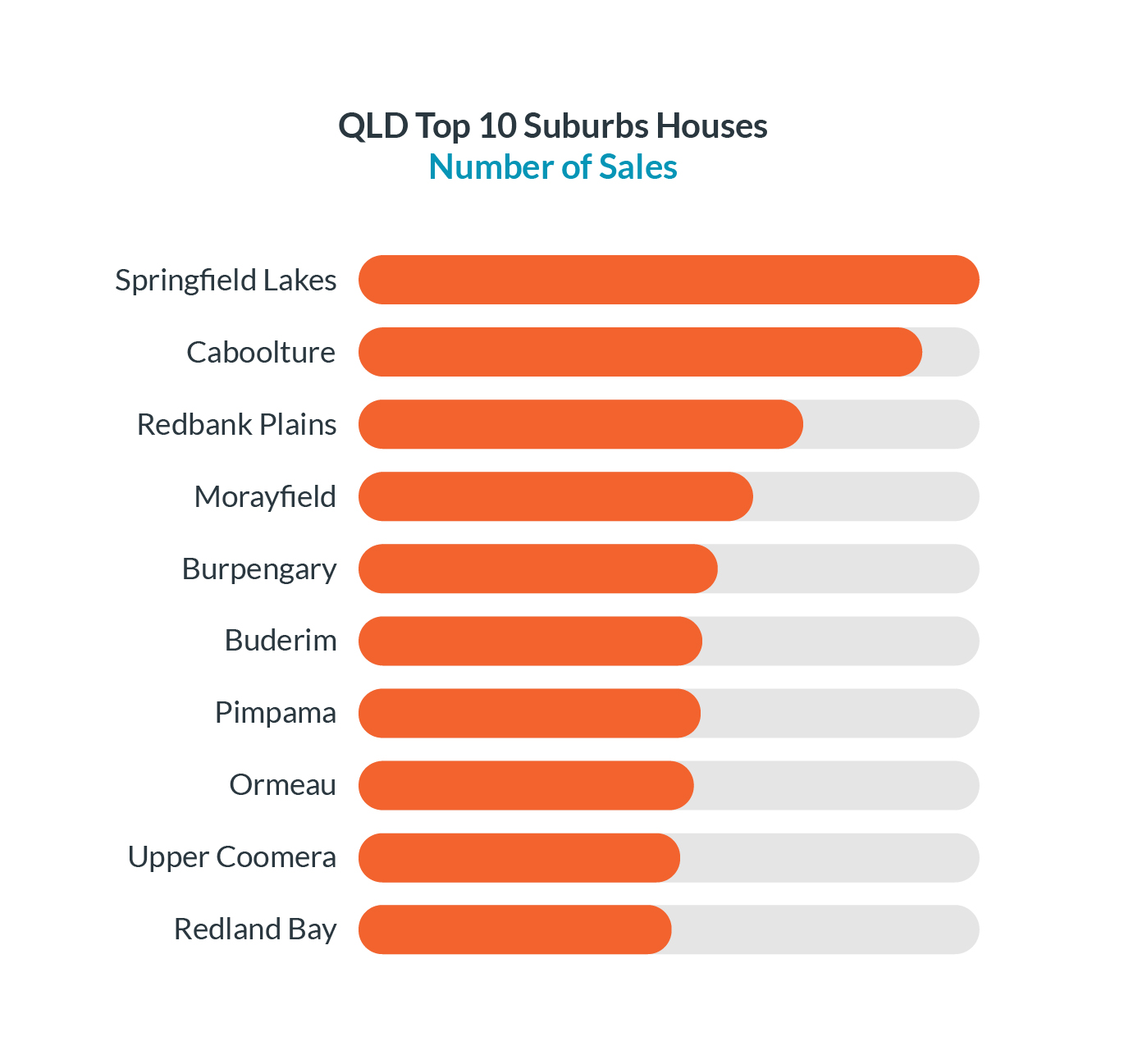

Discover leading edge property insights

Access InfoTrack directly inside Claude Cowork